您当前的位置:首页>论文资料>全面营改增政策对轨道交通业的影响及对策

内容简介

都市快轨交通・第30卷第4期2017年8月

都市快轨交通・第30卷第4期2017年8月doi:10. 3969/j. issn. 1672 -6073. 2017. 04, 005

全面营改增政策

《快轨论坛

对轨道交通业的影响及对策

曹永

(南京地铁建设有限责任公司,南京210008)

摘要:在介绍营改增历史发展背景及意义基础上,详细分析全面营改增对企业不同发展阶段、不同项目建设管理模式、地铁工程造价及固定资产等3个方面的影响,并重点研究建筑施工合同的税务测算以及目前施工合同中存在的涉税风险及应对策略。全面营改增政策允许将新增不动产所含的增值税进行抵扣,对于轨道交通企业而言,在建设项目招投标、合同签订环节均需要提前做好纳税筹划和风险防范,预先设置数据指标,测试不同方式下的最终税负,及时调整招投标及合同要求,以适应营改增的变化,寻求最佳项目施工方案,保证增值税进项税合法有效地进行抵扣。

关键词:轨道交通企业;营改增:施工合同;应对策略

中图分类号:U231;F810.422

文献标志码:A

文章编号:1672-6073(2017)04-0024-04

InfluencesofReplacingBusinessTaxwithValue-added TaxonRailTransitBusinessesandtheCountermeasures

CAOYong

(Nanjing Metro Construction Co., Ltd., Nanjing 210008)

Abstract: The influences of replacing business tax with value-added tax were discussed in terms of different development stages of rail transit enterprises, different metro project management modes as well as metro project costs and fixed assets. Moreover, contract tax calculation and tax-related risks and countermeasures of construction contract were investigated. New real estate has been included into the deduction scope since the business tax was replaced with the value-added tax( VAT) . For the rail transport businesses, tax planning and risk prevention should be analyzed before bidding and signing of construction project contracts,and data indicators will be set and the final tax burden will be measured in different ways. Thus, bidding and contract requirements will be adjusted timely to adapt to the policy change of replacing the business tax with the value-added tax. Rail transport busi-nesses will find the best project construction program to guarantee that the VAT input tax can be used to deduct VAT output le-gally and effectively.

Keywords: rail transport businesses; replace the business tax with the value-added tax; construction contract; countermeasures

1

营改增背景及意义

2012年初,上海率先开展营业税改征增值税(以

下简称营改增)部分试点,试点行业包括交通运输业和部分现代服务业;随后陆续扩大试点范围,逐步增加试点城市和行业,2016年3月,财政部、国家税务总局下发文件规定:自2016年5月1日起,建筑房地产、金融保险、生活服务业也纳人营改增试点范围【0]。营改增

收稿日期:2016-08-23修回日期:2016-09-07

作者简介:曹永,女,硕士,中级会计师,经济师,专业方向:财务理论

与方法,caoyong1125@126.com

24URBAN RAPID RAIL TRANSIT

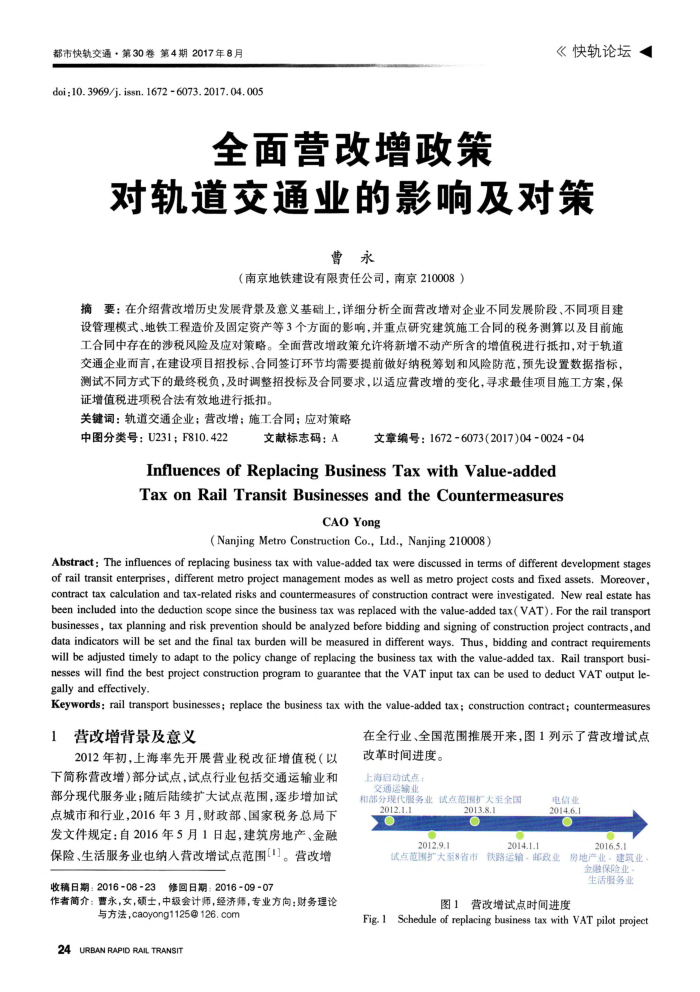

在全行业、全国范围推展开来,图1列示了营改增试点

改革时间进度。上海启动试点:交通运输业

和部分现代服务业试点范围扩大至全国

Z1O2

2012.9.1

2013.8.

2014.1.1

电信业 2014.6.1

2016.5.1

试点范围扩大至8省市

铁路运输、邮政业

房地产业、建筑业

金融保险业生活服务业

营改增试点时间进度

图1

Fig. 1 Schedule of replacing business tax with VAT pilot project

上一章:日本大阪轨道交通系统简析及启示

下一章:有轨电车可持续发展研究